1. Introduction: Winning on Facts, Losing on Rules

Correct facts can still lose when settlement depends on rule interpretation.

TL;DR

- Polymarket users are not always trading the headline event. They are trading the event plus the market rules, evidence deadline, source hierarchy, clarification history, and UMA dispute path.

- The Strategy Bitcoin-sale dispute is the cleanest anchor case: the company later disclosed a sale during the market window, but the market settled around whether eligible confirmation existed before the deadline.

- "OGs" in this essay means experienced, repeat prediction-market participants who know the rule layer, precedent layer, and oracle layer. Their edge is often operational rather than mystical.

- The word "slaughter" is used as a structural metaphor: when one side reads the visible question and the other side reads the effective contract, losses can look less like bad forecasting and more like information asymmetry.

- Rule ambiguity, post-hoc clarifications, token-weighted voting, and execution infrastructure are separate mechanisms. They often compound, but they should not be collapsed into one generic claim of "manipulation."

- The practical takeaway is methodological: market odds should be read as rule-conditioned probabilities, not raw probabilities detached from settlement mechanics.

Before the knife comes out, a few words need plain-English meanings.

UMA is the oracle protocol behind many disputed Polymarket resolutions. DVM, its Data Verification Mechanism, is the token-holder vote that can decide a challenged answer. An 8-K is a US public-company filing; in the Strategy case, it became the receipt everyone argued over. PnL means profit and loss. Semantic fungibility means two markets that sound equivalent may still pay out differently if their rules are not equivalent. And OGs are not wizards. They are repeat players who read the rules, remember precedent, and know where the trapdoors usually sit.

1.1 The Strategy BTC Dispute

This was the market: a simple question on the surface, a settlement fight underneath.

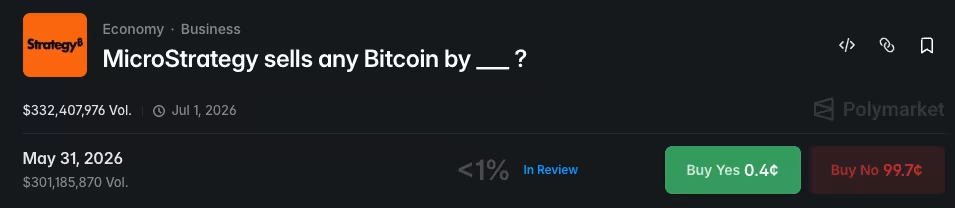

The market looked almost insultingly simple: would Strategy, formerly MicroStrategy, sell any Bitcoin by May 31, 2026?

Then the filing arrived. Strategy's June 1 8-K said it had sold 32 BTC between May 26 and May 31. If you were reading the world, that looked like YES. If you were reading the settlement machine, the next question was nastier: did the proof arrive inside the eligible window?

That is the whole article in miniature. One group thought the market was asking, "Did the sale happen?" Another group understood the more profitable question: "What will the rules count as admissible evidence?" Galaxy Research described the dispute as a case where traders could be right about the event and still lose because evidence timing mattered.1 Oak Research argued that Polymarket had other possible choices, including voiding or treating post-deadline entrants separately, but the final outcome still contradicted many traders' event-level reading.2

The sequence was not complicated. That is what made it so brutal.

- Before May 31, traders saw a market about whether Strategy sold Bitcoin by the deadline.

- On June 1, Strategy's 8-K disclosed a 32 BTC sale during the May 26-31 period.

- After the filing, Polymarket's additional context made confirmation timing central.

- The reported UMA-backed outcome upheld NO.

The lesson is small enough to fit on a sticky note: the market was not only about the sale. It was about what kind of proof counted, and when that proof had to arrive.

1.2 The Real Object of Analysis

New players read a market like a headline. Experienced players read it like a contract with a fuse attached.

That one habit changes everything. The headline asks, "Will this happen?" The rules ask, "What exact thing counts, according to which source, before which deadline, under which dispute process?" Those are not the same question. They only look the same when the market is calm.

Then a dispute starts. Suddenly the nice clean price chart turns into a courtroom, a rules committee, and a governance vote wearing a trench coat. The beginner keeps arguing about reality. The veteran asks a colder question: what will the resolver accept as truth?

That is the slaughterhouse. Not because every disputed market is malicious. Because the interface can make two very different games look like one. One side trades the visible question. The other trades the settlement layer.

2. Settlement Ambiguity: Titles Are Summaries, Rules Are Contracts

Most settlement surprises fit into time, source, or degree traps.

2.1 Market Titles Are Summaries; Rules Are Contracts

The visible title is a compression layer. It makes a market readable, shareable, and tradeable. It is not always the operative settlement text that resolves the market.

The Zelenskyy suit market illustrates the problem. The public question sounded almost comically simple: did Volodymyr Zelenskyy wear a suit? People saw a black jacket, matching trousers, media descriptions, and thought: sure, that is a suit. Normal human behavior. Also dangerous.

The dispute turned on a stricter definition of what counted as a suit and whether credible reporting created enough consensus. WIRED covered the backlash as a rebellion against a market where common-language meaning and settlement meaning diverged.3 The point is not menswear. The point is that one ordinary word became a payout boundary.

This is not unique to clothing. Prediction markets routinely use ordinary words such as "significant," "official," "material," "ban," "launch," "first," "agree," and "confirm." Those words are efficient in headlines and dangerous in contracts.

2.2 Time, Source, and Degree Traps

Ambiguity is not random. It has favorite hiding places.

Time words are one. "By," "before," "announced," and "confirmed" look interchangeable until money is on the table. Then one word decides whether the event date matters or the confirmation date matters.

Source words are another. "Official," "credible reporting," and "consensus" sound reassuring. They are only reassuring if the rule says which source wins when sources disagree.

Degree words are the sneakiest. "Any," "significant," "material," and "suit" feel obvious until someone has a financial reason to make them less obvious.

Scope words finish the job. "Speech," "deal," "ban," and "launch" can point to different slices of the same real-world event. The broader the headline, the more room there is for the settlement text to surprise you.

The Strategy case is a time/evidence trap. The Zelenskyy case is a degree/definition trap. TikTok ban markets are scope/legal-status traps. Ukraine mineral-agreement disputes are rule-plus-governance traps. The surface stories are different; the cognitive error is the same: users price the event while the market settles the rule.

2.3 Source Hierarchy Is Not a Detail

Settlement rules can diverge from the event users think they are pricing.

Source traps appear when a rule names multiple evidence classes without a clear ranking. Official documents, credible reporting, agency notices, court records, platform clarifications, and oracle votes can point in different directions. DefiRate's settlement explainer frames this as a contract-design problem: event contracts need explicit resolution sources because small source differences can produce different outcomes.4

A well-formed market should answer these questions before trading begins:

- Which source is primary?

- Which source is fallback?

- What happens if the primary source is silent?

- What happens if credible reporting conflicts with an official source?

- Can a later official filing prove an earlier event?

- Can the platform issue additional context after positions have been built?

Without that hierarchy, the market is not a clean forecast. It is an interpretation market.

2.4 How Experienced Participants Position

Experienced participants do not need secret magic. Their advantage is often boring, which is why it works.

They read the full rule text. They circle verbs. They treat time words like landmines. They search similar markets. They watch the dispute path. They compare venues. They respect liquidity and spreads because being right and getting paid are cousins, not twins.

That is why "OG" is not just a social label. It describes a different reading discipline. New participants read the claim. OGs read the contract plus the institution that will interpret it.

2.5 Cross-Platform Semantics

The same event can resolve differently under different rulebooks.

Two markets can ask what appears to be the same question and still not be substitutes. One may require an official notice; another may require an actual operational shutdown. One may resolve on statute; another on enforcement; another on user availability. Academic work on semantic non-fungibility formalizes this problem: contracts that look similar to humans can violate the law of one price when settlement semantics differ.5

The practical implication is severe. A price is not a raw probability. It is a rule-conditioned probability. Anyone quoting market odds without reading the rulebook is quoting a number without its measurement instrument.

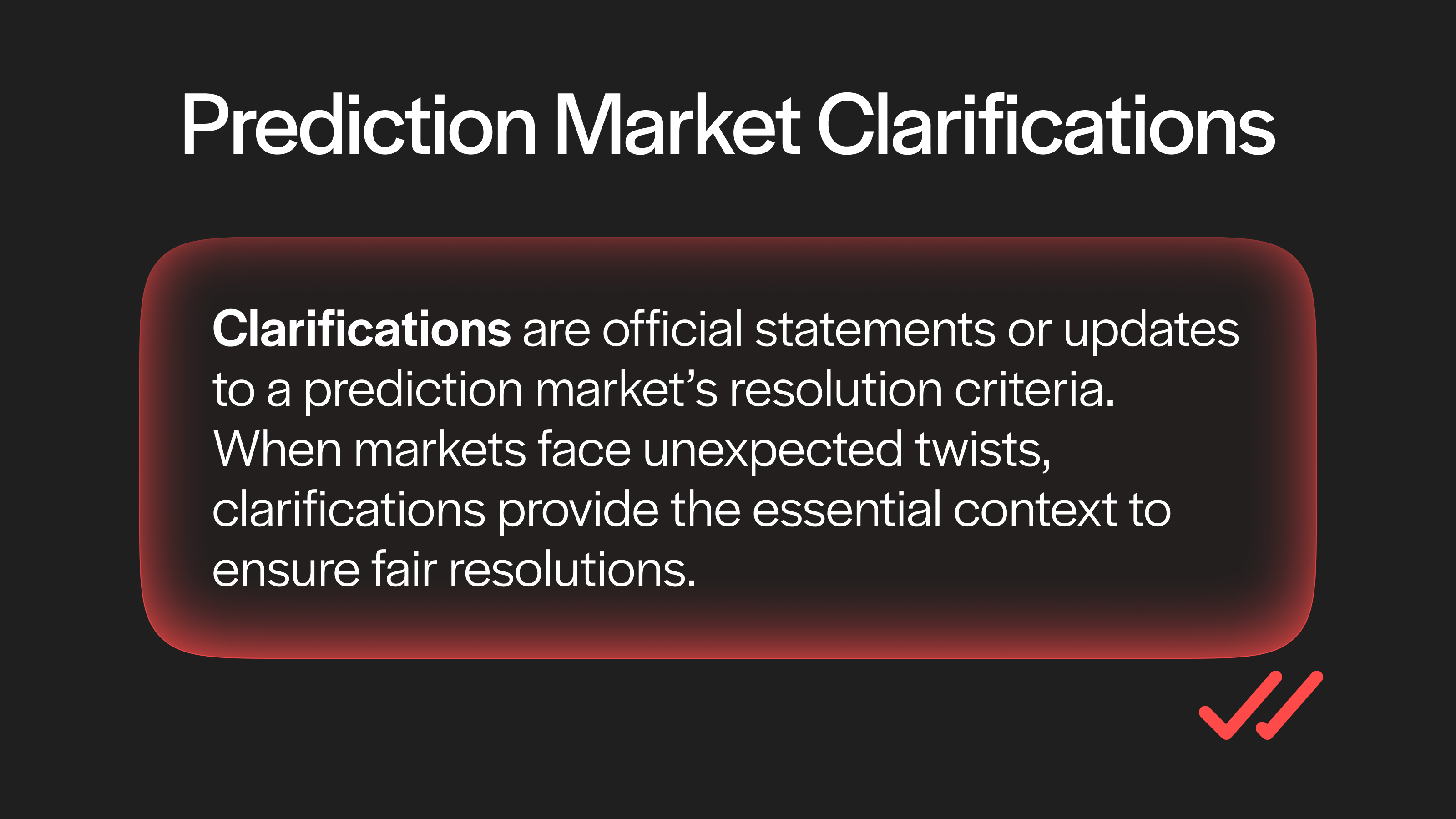

3. Clarification Risk: The Moving Goalposts

Clarifications are useful when rules are incomplete, but they also change the risk surface.

3.1 Clarifications Are Guidance Until They Become the Game

Additional context can become the operative rule voters use to resolve ambiguity.

UMA describes prediction-market clarifications as a way to guide resolution when original wording leaves ambiguity.6 In principle, this is reasonable. Markets are created before every edge case is known, and some interpretive layer can prevent chaos.

The risk is timing. A clarification issued before a market opens is part of the contract. A clarification issued after capital has entered can feel like interpretation to the platform and a rule change to the trader. A clarification issued during a dispute can become even more powerful because voters are looking for a coordination signal.

The relevant question is not whether clarifications are legitimate in theory. The relevant question is when they become binding enough that they should be priced as part of the original market.

3.2 Strategy as a Clarification Case

The Strategy dispute matters here because it shows how a market can move from an event standard to a confirmation standard. The dispute did not merely ask whether Strategy sold Bitcoin. It asked whether the evidence that Strategy sold Bitcoin satisfied the market's timing and source requirements.

That is a different asset. A trader buying YES after reading the company filing was effectively buying the event. A trader buying NO after reading the clarification was buying the resolver's likely interpretation. The same order book hosted both trades.

This distinction is why serious market infrastructure should show rule history and clarification history as first-class data. A price chart without a rule-diff timeline is incomplete.

3.3 TikTok as a Scope and Legal-Status Case

Legal status, service availability, and settlement can point in different directions.

TikTok ban markets show a different version of the same problem. Reports described user backlash after a ban-related market resolved YES even though access, enforcement, legal status, and user availability were contested.7

One reading focused on a legal trigger. Another focused on whether the service was actually banned from being downloaded or used by most Americans. Another focused on later executive action and practical availability.

That is the trap. "Banned" sounds like one event. It can actually mean statute, enforcement, app-store status, or lived user access. If the rule does not pick one, traders will pick the one that feels obvious to them. Settlement may pick another.

This case should make designers uncomfortable. A market can be technically defensible and still feel illegible to users if the rule does not name the decisive institutional fact.

3.4 Regulated Comparison: Locked Rules vs Flexible Context

Filed rules reduce the space for informal reinterpretation.

Regulated event-contract venues generally operate with more formal rule filings. DefiRate's reporting on Kalshi's CFTC-filed death-settlement rule shows the trade-off: formal rules can be slower and narrower, but they reduce post-hoc interpretation space.8

| Model | Strength | Cost |

|---|---|---|

| Filed deterministic rules | Predictable settlement and clearer user recourse. | Slower market creation and narrower event coverage. |

| Clarification-heavy rules | Fast iteration and broad market coverage. | Higher interpretation risk and more dependence on platform guidance. |

| Token-voted oracle | Decentralized-looking dispute surface. | Voter concentration, incentive conflicts, and governance attacks. |

Polymarket's advantage is speed and breadth. Its risk is that speed and breadth move ambiguity from product creation into settlement. That is acceptable only if the ambiguity is visible to users before they trade.

4. UMA Voting Power and Governance Risk

In token-weighted voting, capital weight can become settlement power.

4.1 The Dispute Path

UMA's optimistic oracle design starts from a useful premise: most answers do not need a full vote. A proposer submits an answer. If no one challenges it during the liveness window, the answer can stand. If someone disputes it, the issue escalates to UMA's Data Verification Mechanism, where token holders vote.9

The flow is easy to say and hard to trust blindly.

First, someone proposes an answer. Then there is a challenge window. If nobody challenges, the answer passes. If someone does challenge, the dispute goes to token-holder voting. After that, the market receives a final answer, and users experience it as a clean YES or NO even if the path there was interpretive, messy, and political.

This is where the shiny phrase "oracle resolved" can hide a lot of machinery. Who proposed? Who challenged? Who voted? Who had exposure? Which answer did the platform's clarification make easier to defend?

The design works best when disputes are rare, stakes are modest relative to oracle security, voters are economically aligned with truth, and no participant can cheaply buy influence. Prediction-market disputes stress every one of those assumptions.

4.2 Concentration and Conflict Are Not Side Issues

A small set of large voters can heavily influence disputed outcomes.

Reporting in 2026 highlighted concentration among UMA voters deciding Polymarket disputes.10 The reported pattern was not merely "some whales exist"; the concern was that a small number of wallets could account for a large share of votes in disputed markets. Concentration alone does not prove manipulation. It does change the institutional model. A dispute can start to look less like a broad public jury adjudicating truth and more like a concentrated governance process whose voters may have their own incentives, exposure, or coordination channels.

Conflict-of-interest reporting made the concern sharper. Crypto Briefing summarized WSJ-linked analysis alleging that some voters in disputed markets could be linked to Polymarket trading accounts and, in some cases, held economic exposure to the outcomes they helped decide.11 Treat that as reported allegation unless independently verified in a given dispute. Even then, it changes the reading standard.

If voting power is concentrated, a few wallets can matter too much. If voters have market exposure, the judge may also be holding a ticket. If public dispute channels coordinate expectations, smaller voters may follow the expected majority. If the penalty system rewards being with the majority more than being independently right, truth has to fight game theory in a parking lot.

In a normal legal setting, adjudicator conflicts would be a central issue. In prediction markets, they are often treated as an implementation detail. They are not.

4.3 Ukraine Mineral Agreement: The Governance Attack Question

The same actors can appear on both sides of the judging table.

The Ukraine mineral agreement market is the clearest governance-risk case. Reports described a market where many users expected NO because no formal agreement had been signed, yet voting weight pushed the resolution toward YES.12 The Block reported Polymarket's statement that the situation was unprecedented and involved a UMA whale attempting to hijack a market's resolution.13

The disputed issue was whether statements or preliminary actions counted as agreement. The reported outcome was YES. The platform framed the situation as unprecedented but did not treat it as a normal market failure requiring refunds. That combination matters: even when users think the rule points one way, a token-weighted resolution process can introduce a second battlefield.

This case is useful because it isolates governance risk rather than ordinary rule ambiguity. The point is specific: token-weighted settlement means that the effective truth function depends on who holds voting power and what incentives they face.

4.4 Barron/DJT and the Exception Problem

There are also counterexamples. Polymarket reversed or rejected an UMA-linked decision in the Barron Trump DJT-token dispute, showing that platform-level judgment can appear after an oracle result.14

That exception cuts both ways. On one hand, it shows that a bad oracle outcome can be corrected. On the other hand, it weakens the simple story that the oracle is final, neutral, and beyond platform discretion. If the platform can distance itself from a result in one case, users will ask why it cannot do so in another.

The real design question is not "centralized or decentralized?" It is: who has final interpretation authority, under what conditions, with what transparency, and with what recourse for users who relied on the original rules?

5. The Data: Structural Losses, Profit Concentration, and Arbitrage

Losses concentrate when information and execution advantages compound.

5.1 PnL Distribution

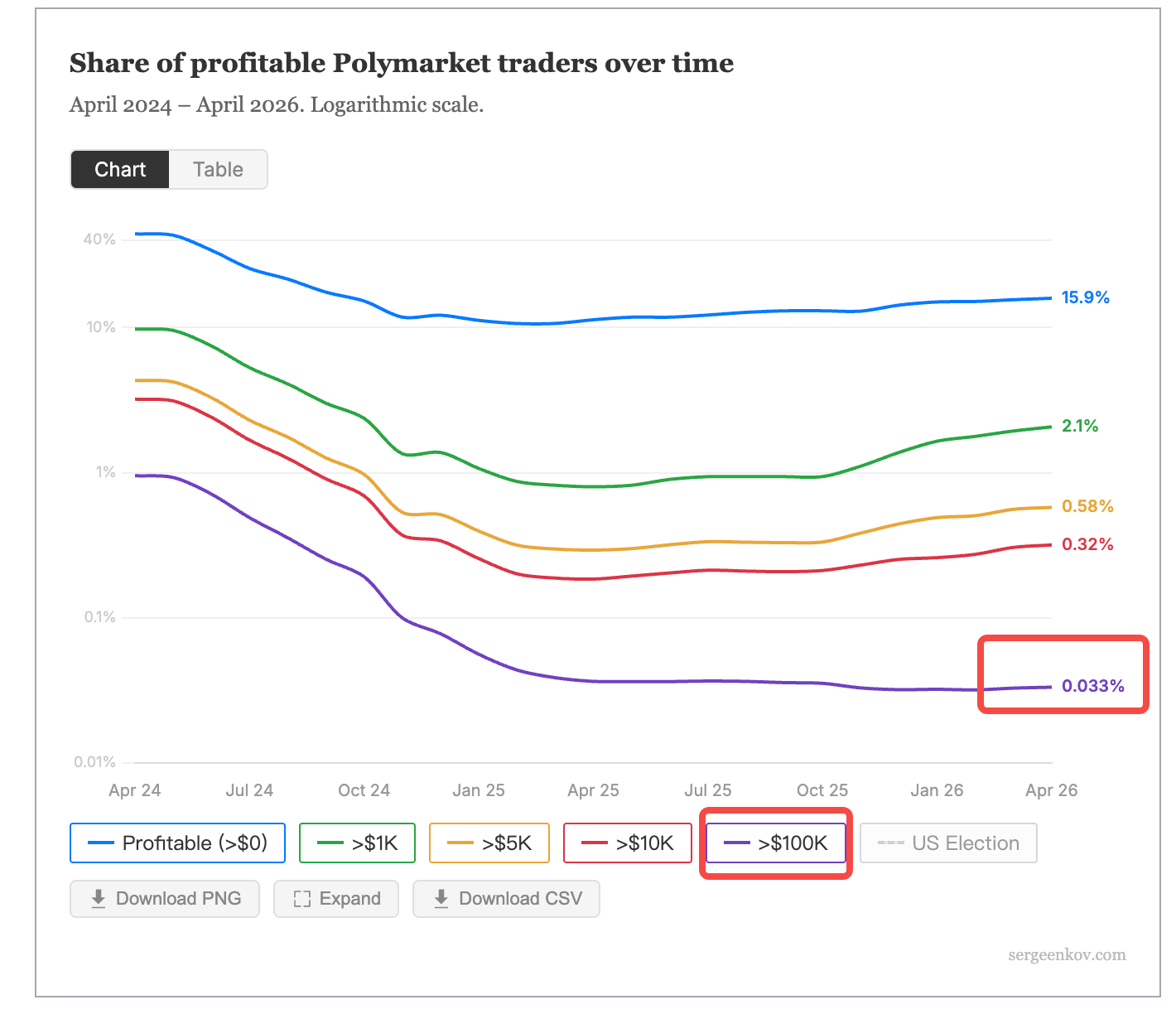

Trader-level PnL data shows a steep distribution rather than a casual game of chance.

Several analyses reported that most Polymarket wallets lose money and that profits concentrate heavily among a small minority.15 One cited analysis put the losing-wallet share at 84%, which is why the exact PnL methodology matters. The precise numbers depend on whether split/merge operations are counted, how inactive wallets are treated, and whether the analysis separates market-making from directional trading.

But you do not need to worship one number to see the shape of the thing. Many wallets lose. A small group wins big. Some profitable runs do not last. Spreads quietly tax the impatient. Disputes create volatility that looks terrifying to beginners and useful to specialists.

This is how edge compounds. First you read the rules better. Then you execute better. Then you understand the oracle better. Then, while everyone else is yelling "but the event happened," you are already asking the only question that pays: what will count?

The data does not prove that every loss is unfair. It does prove that prediction markets are not merely games of opinion accuracy. The payoff function includes rule interpretation, execution, latency, liquidity, and dispute competence.

5.2 Arbitrage and Semantic Non-Fungibility

Research on UMA-resolved markets makes dispute resolution analyzable.

Academic work on prediction-market arbitrage found structural pricing errors and exploitable relationships across related contracts.16 Another paper studied UMA-resolved Polymarket disputes and treated oracle outcomes as a system that can be analyzed rather than as unstructured folklore.17

This matters because it changes the meaning of "edge." If related markets violate semantic fungibility, a participant can profit without a better view of the underlying event. If dispute outcomes correlate with rule wording, precedent, and clarification features, a participant can profit by understanding settlement behavior rather than reality itself.

That is the deeper criticism. A prediction market that rewards better world models is one thing. A market that rewards better interpretation of hidden rule precedent is another.

5.3 Disputes as Liquidity Events

Disputed markets often attract attention, capital, and volatility. For casual users, a dispute is a warning sign. For experienced participants, it can become a new market: not "what happened?" but "what will the oracle count?"

This is why the Strategy case is so revealing. Once the 8-K was public and the clarification appeared, the market stopped being a simple Bitcoin-sale question. It became a live instrument for pricing whether voters would follow an event-time or confirmation-time interpretation. That transition is invisible if the interface only shows price.

Before the dispute, users price the underlying event. During the dispute, they price resolver behavior. Before the dispute, evidence means filings, news, and on-chain data. During the dispute, evidence also means clarifications, dispute arguments, and voter expectations. The market starts as a forecast and mutates into a legal-oracle microstructure trade.

If the product does not expose that transition, new users are structurally late.

5.4 What the Data Does and Does Not Prove

The data supports four narrower conclusions:

- Prediction-market prices include settlement mechanics, not only event beliefs.

- Profit concentrates where rule literacy, execution, and infrastructure compound.

- Dispute resolution is a market object that can be studied and anticipated.

- New participants who ignore settlement mechanics are underpricing risk.

The data does not prove that every profitable participant is malicious, every disputed outcome is wrong, or every loss is a platform failure. Overclaiming would weaken the argument. The stronger and more useful claim is that settlement risk is real, systematic, and under-displayed.

6. The Veteran Player's Arsenal

The edge is usually mundane: read more carefully, earlier, and with better context.

6.1 The Arsenal Is Mostly Process

Experienced users do not need a conspiracy. They need a process that new users do not run.

They read full rules instead of titles. They separate the event date from the confirmation date. They ask which source wins if sources conflict. They remember similar markets. They watch clarifications. They notice when a dispute turns an event forecast into an oracle forecast.

And then they do the most underrated thing in trading: they do not confuse being right with getting paid.

The edge is not romantic. It is operational. The unfairness comes from invisibility: the interface makes the market look like a simple question, while the actual trade is a stack of institutional dependencies.

6.2 A Practical Rule-Reading Workflow

Good market reading starts with the rulebook, not the headline.

Before using a market as a signal, a serious reader should be able to answer:

- What exact sentence controls settlement?

- Which terms are undefined?

- Which source wins if sources conflict?

- Is the deadline about the event, public announcement, reporting, confirmation, or availability?

- Has a similar market been clarified or disputed before?

- Can additional context be issued after the market is already liquid?

- What happens if the answer is challenged?

- Who benefits financially from each disputed outcome?

- How much liquidity is available, and how wide is the spread?

- What evidence would make the opposite side rational?

If this checklist feels excessive, that is the point. The market may still be useful as a public signal. It is not a low-friction bet on the headline.

6.3 Infrastructure Implication

For research infrastructure builders, the lesson is clear: price alone is not enough. A useful prediction-market research surface should show:

- The market question and full rule text.

- Deadline semantics and key verbs.

- Primary and fallback sources.

- Clarification history with timestamps.

- Similar-market precedent.

- Open dispute status and challenge windows.

- UMA vote concentration and known governance-risk indicators where available.

- Cross-market and cross-venue semantic differences.

- Liquidity, spread, and capital-lockup warnings.

- A separation between event movement and settlement-interpretation movement.

That is the infrastructure gap this essay identifies. The reader should see whether price moved because the world changed, because evidence changed, or because the settlement interpretation changed.

7. The New Player's Hidden Risk Surface

The interface can make a contract feel like a headline.

7.1 The UX Teaches the Wrong Reading Habit

Prediction-market interfaces are optimized for fast comprehension: a short question, two prices, a chart, a deadline, and a button. That is good product design for liquidity. It is bad product design for settlement literacy.

The new player sees a clean binary question and asks, "Will this happen?" The veteran asks, "What exact evidence, from which source, by what time, will make the resolver count this as having happened?"

Those are different questions. A UI that does not make the difference visible is not neutral. It trains users to underread the contract.

7.2 Why the Loss Feels Like Betrayal

Many disputed losses feel worse than ordinary trading losses because the losing user does not experience them as failed predictions. They experience them as successful predictions that were later rejected by an unfamiliar rule layer.

The Strategy case is painful for that reason: the user's mental model was "the company sold Bitcoin before the deadline." The settlement model was "confirmation did not qualify inside the market timeframe." The user did not merely lose a trade. The user discovered a second game after playing the first.

The Zelenskyy case is painful for a similar reason: the user's mental model was common-language visual classification. The settlement model was definitional sufficiency under dispute. The visible world and the accepted contract boundary separated.

The Ukraine mineral case is painful in a third way: the user's mental model was rule reading, while the settlement model exposed governance power. When a token-weighted vote can decide the answer, users are not only pricing facts. They are pricing the electorate.

7.3 Risk Controls for New Participants

A disciplined new participant should treat ambiguous markets as higher-risk instruments, even when the event looks obvious.

Read the full rules before entering. Identify the decisive source. Check whether later evidence will count. Search similar resolved markets. Avoid markets already in interpretive dispute unless that is the trade you actually want. Size positions as if a dispute can lock capital and invert the obvious answer. And never mistake high volume for safety. High volume sometimes means everyone is crowded around the same hole in the floor.

These controls do not guarantee profit. They prevent the most avoidable category of loss: being right about the world while wrong about the contract.

8. Bugs for New Players, Features for OGs

The industry is splitting between deterministic settlement and interpretation-heavy markets.

8.1 Why Ambiguity Persists

From a new participant's perspective, ambiguity looks like a bug: the product asked one thing, reality seemed to answer, and settlement went another way. From an experienced participant's perspective, the same ambiguity can be a feature because it creates edge for people who understand precedent, timing, source hierarchy, and dispute incentives.

Ambiguity persists because it has real benefits:

- It allows faster market creation.

- It covers events that deterministic feeds cannot settle.

- It lets platforms handle edge cases without pre-writing every scenario.

- It creates liquidity and attention during disputes.

- It rewards participants who specialize in resolution mechanics.

The same properties that make the system flexible also make it dangerous for casual users. Flexibility is not free. Its cost is paid in interpretation risk.

8.2 The Physical Data Lesson

Reports about the hair-dryer weather-market episode add a final layer to the argument.1819 This was not a rule-definition case, a clarification case, or a token-vote case. It was a data-generation case: a physical sensor could become the settlement surface.

That is the broader lesson. Every prediction market has a place where reality enters the machine. Sometimes it is a filing. Sometimes it is media consensus. Sometimes it is a platform clarification. Sometimes it is UMA voting. Sometimes it is a weather station that apparently needed a bodyguard.

The market becomes real at that surface.

8.3 What a Better System Would Show

A better prediction-market information system would not hide the settlement layer behind the price. It would display:

- A rule-risk summary next to each market.

- A machine-readable source hierarchy.

- A deadline-semantics label: event-time, announcement-time, confirmation-time, or availability-time.

- Clarification diffs with timestamps.

- Similar-market precedent.

- Dispute-state indicators.

- Governance concentration warnings when token voting is active.

- Cross-venue rule differences.

- A clean distinction between event probability and settlement-risk probability.

This is not an anti-market position. It is a pro-market-infrastructure position. Markets become more useful when users understand what the price is measuring.

8.4 Conclusion

Prediction markets can be powerful public instruments. They can aggregate dispersed information, reveal consensus changes, and make belief measurable. But they are not magic truth machines. They are contracts with settlement machinery.

The optimistic oracle becomes an abattoir when one side believes it is trading facts and the other side knows it is trading rule interpretation. The solution is not to pretend ambiguity can disappear. The solution is to make the ambiguity visible, timestamped, searchable, and priced before users discover it through losses.

Until then, the warning is simple: in prediction markets, evidence only matters after the rules decide what evidence counts.

References

-

Strategy sold BTC, Polymarket said NO: Inside the biggest inter-subjective market dispute of 2026 ↩

-

Volodymyr Zelensky's Clothing Has Sparked a Polymarket Rebellion ↩

-

How Polymarket and Kalshi Settle Event Contracts (and Disputes) ↩

-

Semantic Non-Fungibility and Violations of the Law of One Price in Prediction Markets ↩

-

Kalshi Codifies Death Settlement Rule in CFTC Filing Amid Iran Market Backlash ↩

-

Nine Crypto Whales Dominate Polymarket Disputes Worth Billions ↩

-

Polymarket faces scrutiny over dispute resolution system as judges found betting on their own cases ↩

-

Polymarket says governance attack by UMA whale is 'unprecedented' ↩

-

Polymarket reverses Oracle decision on Barron Trump's involvement in DJT meme coin ↩

-

Unravelling the Probabilistic Forest: Arbitrage in Prediction Markets ↩

-

Can LLMs Help Decentralized Dispute Arbitration? A Case Study of UMA-Resolved Markets on Polymarket ↩

-

$119 In, $37,000 Out: The Hair Dryer That Beat Polymarket's Oracle ↩